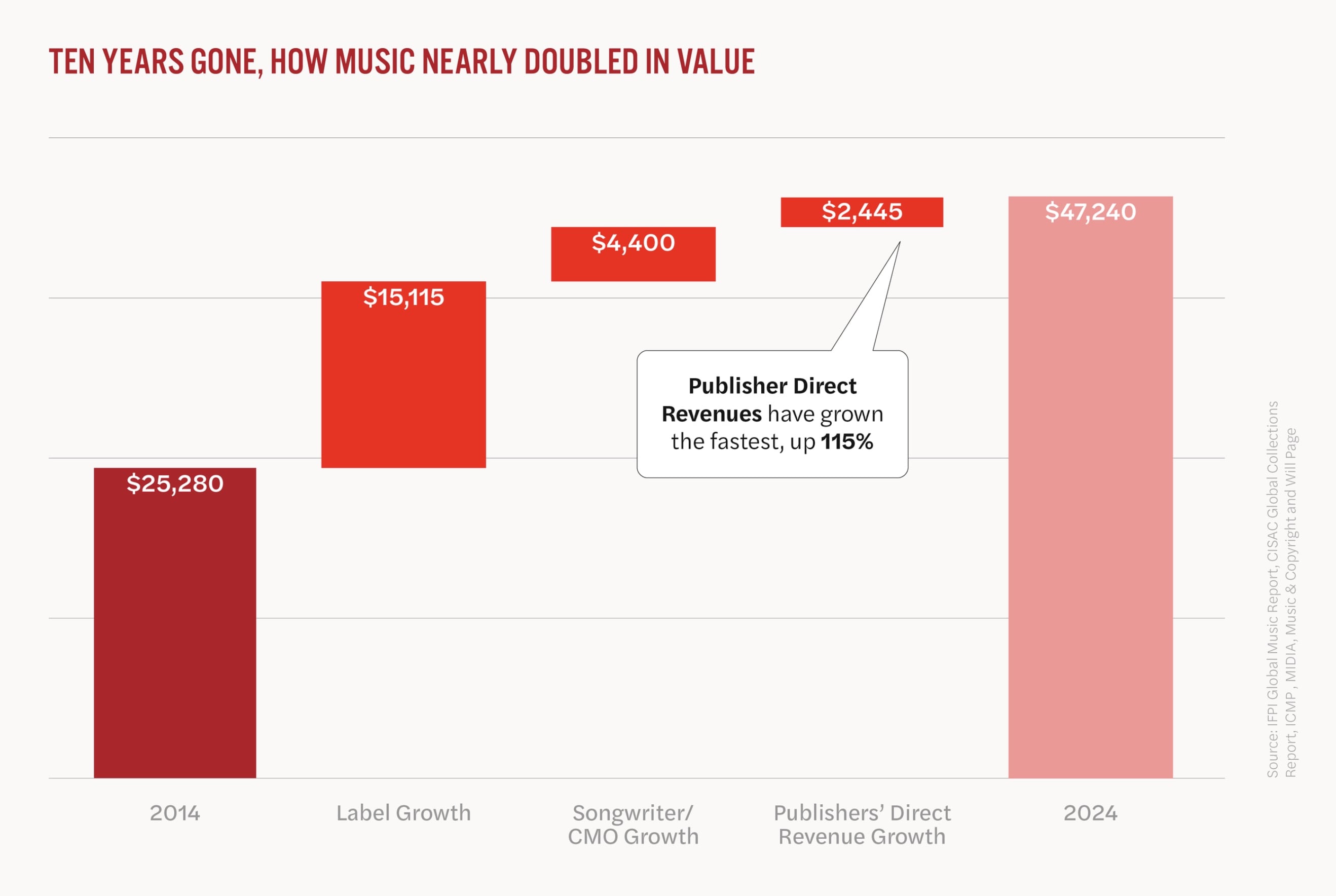

The global value of music copyright (both recordings and compositions) reached a new all-time high of $47.2 billion in 2024.

That’s according to a new report from Will Page, the former Chief Economist at both Spotify and UK collection society PRS for Music, published on Page’s website, Pivotal Economics.

The 2024 figure was up just $2.3 billion (5.2%) on the prior year. According to the report, “growth is slowing largely because this is the first year where the pandemic effects have vanished”.

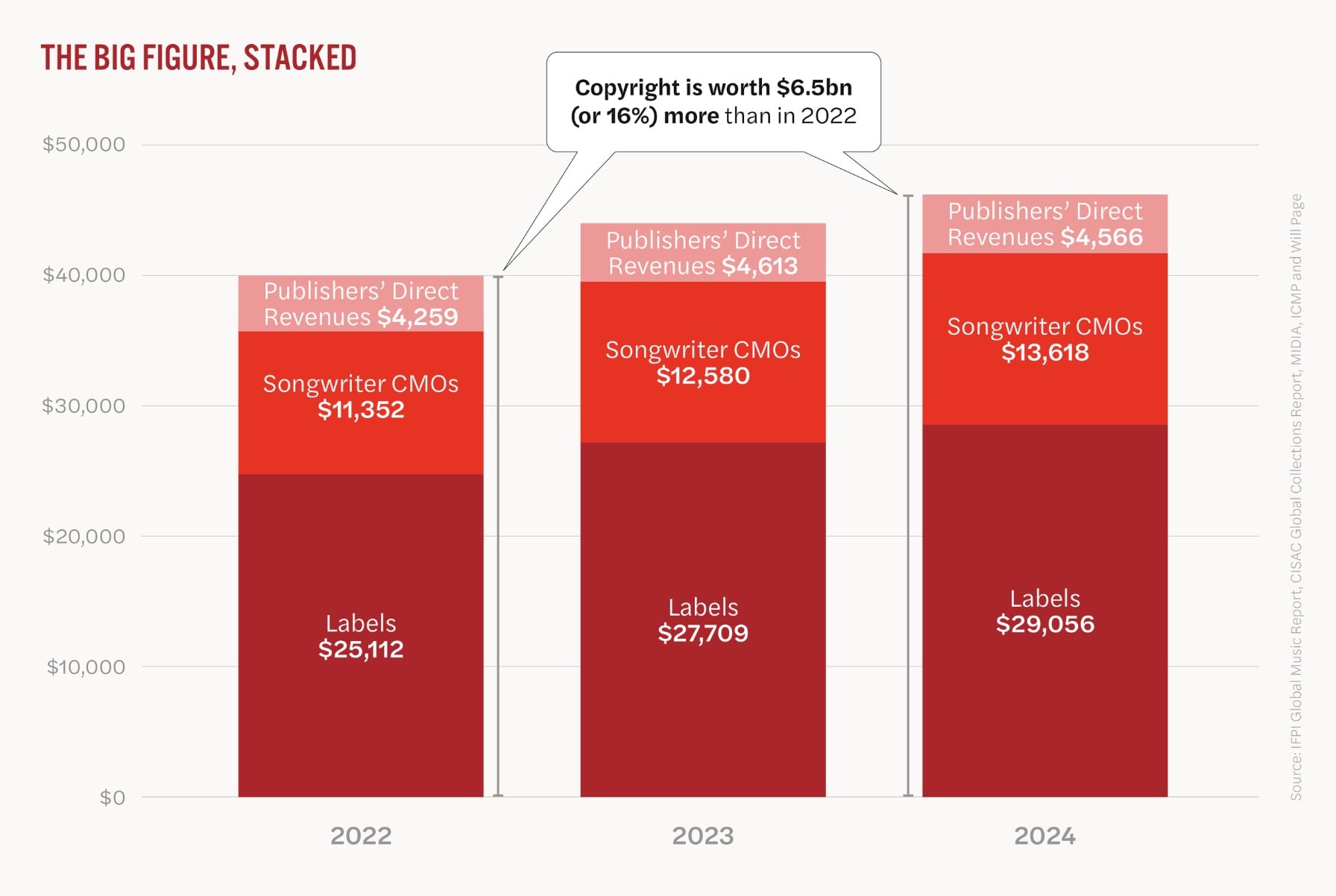

Of that total, $29 billion – or 61% – came from recorded music revenues (up 5% YoY), while $13.6 billion was brought in by collective management organizations (CMOs, up 8% YoY) and $4.6 billion in direct publisher income (down 1% YoY). Thus, compositions brought in 39% of the total.

MBW was first to publish Page’s global value of music copyright report back in 2015, when he calculated the figure at $25 billion for 2014 – making today’s $47.2 billion number a near doubling over the past decade.

Over that ten-year period, the three segments grew at dramatically different rates: CMOs expanded by 50%, labels doubled their revenues, and publishers’ direct revenues swelled by 112%. The report notes that “ICMP has long championed the ability of publishers to license their rights directly, circumventing the constraints of the collective, and this performance supports their argument”.

That growth has been driven by streaming’s continued expansion and the rise of what Page calls “glocalisation” – the phenomenon of domestic market strength reshaping global music economics.

However, Page’s analysis suggests the headline number only tells part of the story. While the industry celebrates crossing this milestone, the economist argues that more significant structural shifts are underway in how that value is being captured and distributed.

Streaming platforms have fundamentally altered the dynamics of music consumption, enabling domestic artists to achieve unprecedented scale in their home markets without necessarily achieving global recognition. This shift has profound implications for how the industry measures success, allocates resources, and projects future growth.

The report also identifies emerging threats and opportunities. From AI music’s potential to simultaneously create and destroy value across different sectors, to measurement gaps that suggest hundreds of millions of dollars remain uncounted, Page’s analysis presents a more complex picture than simple year-over-year growth figures might suggest.

Meanwhile, revenue time-lags between labels and publishers hint at cyclical patterns that could reshape near-term expectations for different stakeholders across the copyright value chain.

Here are five key takeaways from the report:

Photo Credit: ElenaR/Shutterstock

1. The $47.2bn milestone masks a structural shift in how value is captured

While the headline figure shows impressive growth over the past decade, Page argues the more significant story lies in where that value is being generated.

“The glocalisation of the value of copyright reminds us that the big figure that is calculated each year is being allocated across markets differently,” Page writes.

Page highlights trends from three markets, including “relatively small Denmark, medium-sized Korea, and large (or extra large) Brazil.”

In Denmark, the report notes, 16 of the top 20 albums last year were by Danish artists performing in Danish, despite the language being spoken by just 6 million people.

The report continues: “These three winners of glocalisation remind us that more of that value is staying within their domestic markets, as opposed to being repatriated back to international headquarters.”

The shift represents a fundamental departure from the broadcast era. “The free market of streaming has achieved what the regulated market of broadcast failed: domestic prominence,” according to Page.

Unlike traditional radio, which often favored international repertoire, streaming platforms have enabled local artists to dominate their home markets while occasionally breaking through to global charts based purely on domestic demand.

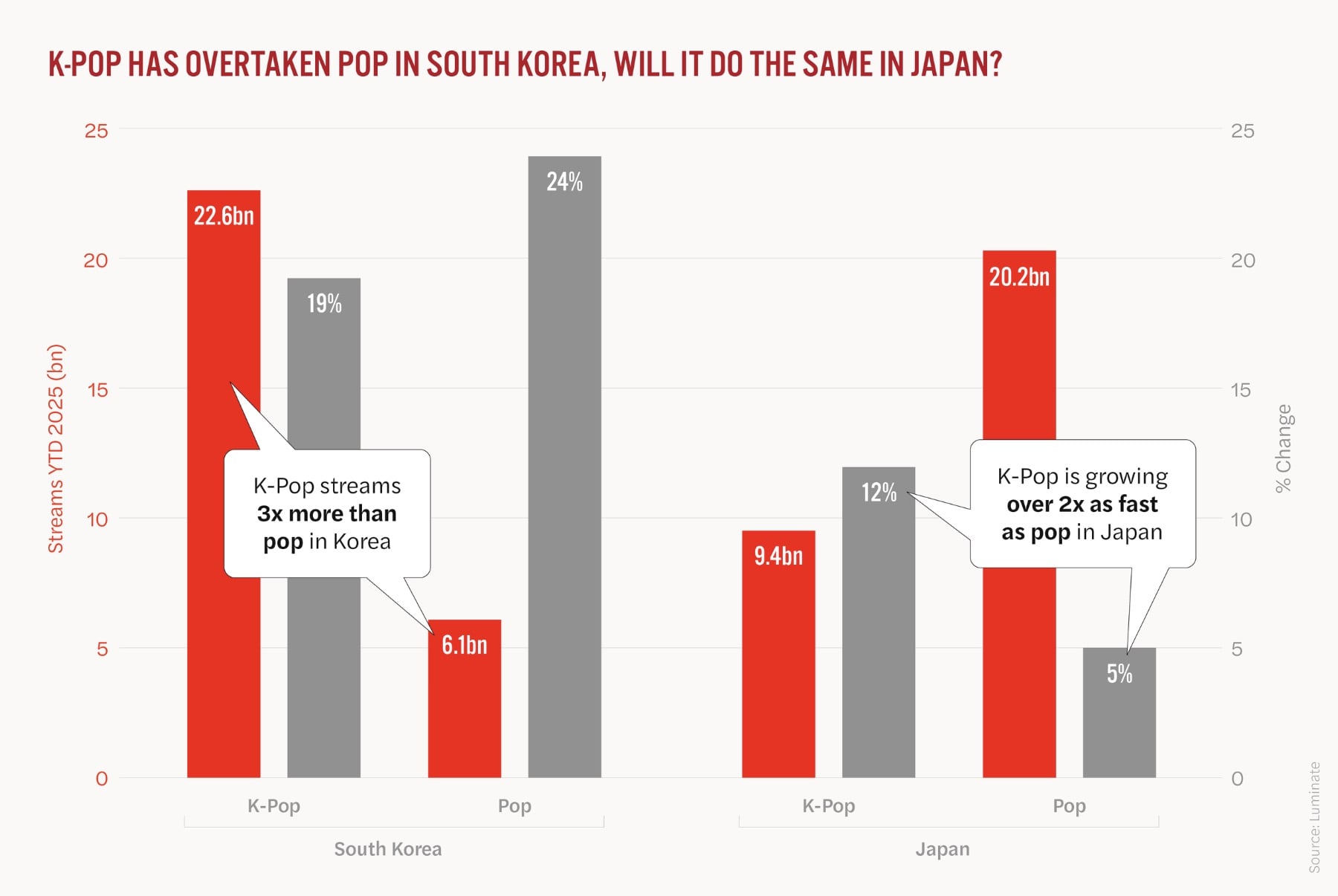

2. K-Pop’s dominance in Japan is blurring genre boundaries

K-Pop has become so dominant in Japan that the genre classification itself is becoming meaningless. “Japan is Korea’s biggest export market, with 14 of the top 100 artists in Japan this year tagged as K-Pop,” Page writes. “The genre of K-Pop has overtaken pop in Korea, whereas it’s half the size of pop in Japan — yet its streams are now growing twice as fast.”

With BTS’s imminent return, Page suggests “we could see a tipping point where K-Pop overtakes pop in Japan.” Should this happen, he notes, “it raises more questions than answers — especially when it comes to syntax of the genre ‘K-Pop’.”

JH Kah, CEO of HYBE Latin America, frames the shift in stark terms: “Tower Records still thrive in Japan, that should tell you a lot! Indeed, an entire floor of their flagship Tokyo store is dedicated to K-Pop, however Japanese label culture suffered from decades of inertia whereas Koreans are inherently more hungry – our mantra is survive and thrive.

“That’s why you are now seeing Japanese labels hiring more Korean executives, and Korean labels going directly into Japan. The lines are getting blurred both on stage and backstage.” Japanese executives have even begun referring to the phenomenon as “J-K Pop,” highlighting the genre’s identity crisis.

3. Brazil’s domestic scale alone is powerful enough to break artists globally

Brazil’s market demonstrates the extreme end of glocalisation. “The YouTube top 100 artist chart for Brazil provides the litmus test for glocalisation: simply scroll from top to bottom and you will not see any international artists — no Spanish, nor English language, not even K-Pop Demon Hunters. It’s all Portuguese,” Page writes.

Yet despite this linguistic isolation, “these Brazilian artists are reaching the top of global charts thanks to (only) local demand.”

Roni Maltz Bin, CEO of Grupo Sua Música, provides striking examples: “Little Love by MC Cabelinho peaked on the Brazilian charts and reached No.2 on the Top Global Debut Album Charts — even though 99.5% of the album’s streams came from inside Brazil. Ditto Evoney Fernandes, who peaked at No.7 despite 97.4% of his streams coming from Brazil.

“Natanzinho Lima debuted in the same week as Bad Bunny and still reached #4 on the Spotify Global chart with 98.3% of all streams coming from Brazil. This shows the strength of the Brazilian market — it can break artists on the global charts even when their artists are only being streamed locally.”

4. AI music poses an asymmetric threat to the industry

“One headwind that needs no introduction is the rise of AI music,” Page writes. “The question on everyone’s lips: will this be complementary or cannibalistic to the existing $47.2 billion business?”

His answer suggests both outcomes are possible simultaneously. “This is where we can revisit our concept of ‘fair division’ and ask if the commercial prospects of recent deals with Suno and Udio might add value to B2C revenues, but wipe out value from the B2B business due to the displacement of production music libraries. If so, the impact of AI may be asymmetric.”

The warning is significant: while the headline $47.2 billion figure might continue growing through consumer-facing AI applications, substantial value could be destroyed in the professional production music sector, creating winners and losers within the same industry ecosystem.

5. The industry is missing hundreds of millions in unmeasured markets

Despite the $47.2 billion figure representing the most comprehensive measurement yet, Page argues significant value remains uncaptured. “The most obvious tailwind, meanwhile, risks of repetition, but remains salient as ever: global needs to mean global,” he writes.

“Of the 196 flags flying outside the United Nations building in New York, our industry yearbooks featured here capture barely a quarter of them. Ceteris paribus, the more we measure, the more value we capture.”

China illustrates the scale of the problem. “With $1.6 billion in recorded music revenues, it’s now ranked fifth in size by the IFPI and will soon overtake both Germany and the UK. But that’s not a complete picture of copyright,” Page notes.

“Industry experts estimate a further 15% should be paid to Chinese publishers — and this isn’t being captured in any of the yearbooks. That’s almost a quarter of a billion dollars currently not being calculated.”

The broader implication is stark: “How many more known-unknown examples like this are there? And if we did know, and measured these markets accordingly, how much bigger might be the global value of music copyright? This is why global needs to mean global when we measure music copyright.”Music Business Worldwide

{kind=link}