MBW Reacts is a series of analytical commentaries from Music Business Worldwide written in response to major recent entertainment events or news stories. Only MBW+ subscribers have unlimited access to these articles. The below article originally appeared in Tim Ingham’s latest MBW+ Review email, issued exclusively to MBW+ subscribers this week.

What’s the world’s biggest subscription streaming market?

If you guessed the USA – the obvious answer – then you’re half-right. And half (very) wrong.

Uncle Sam still leads the world in terms of subscription revenues (at over USD $6 billion annually).

But in terms of the volume of paying subscribers, nowhere can touch China.

China’s top two music streaming providers, Tencent Music Entertainment (TME) and NetEase Cloud Music (NCM), counted around 171 million paying users between them at the close of 2024.

That’s nearly double the volume of subscription streaming accounts in the US at the same juncture: 100 million (source: RIAA).

What’s more, China is growing way faster than the USA.

China added over 25 million paying music subs in 2024, according to senior industry sources.

The USA? Just 3.2 million.

China is also rapidly gaining global market share of subscription streaming revenues.

According to IFPI data, China’s annual subscription trade revenues surpassed USD $1 billion in 2024, up 18.9% YoY.

In doing so, China surpassed Germany to become the world’s third-largest subscription market.

It now looks inevitable that China will leapfrog the world’s second-largest subscription market, the UK, by 2026.

So what’s ‘The China Paradox’?

The meteoric rise of China as a subscription market is obviously a boon for the world’s biggest music rightsholders.

Yet, at the same time, it’s a significant threat.

That’s because Tencent Music and NetEase Cloud Music are increasingly competing with music rightsholders to sign and produce China’s biggest hits.

Get your head around these numbers.

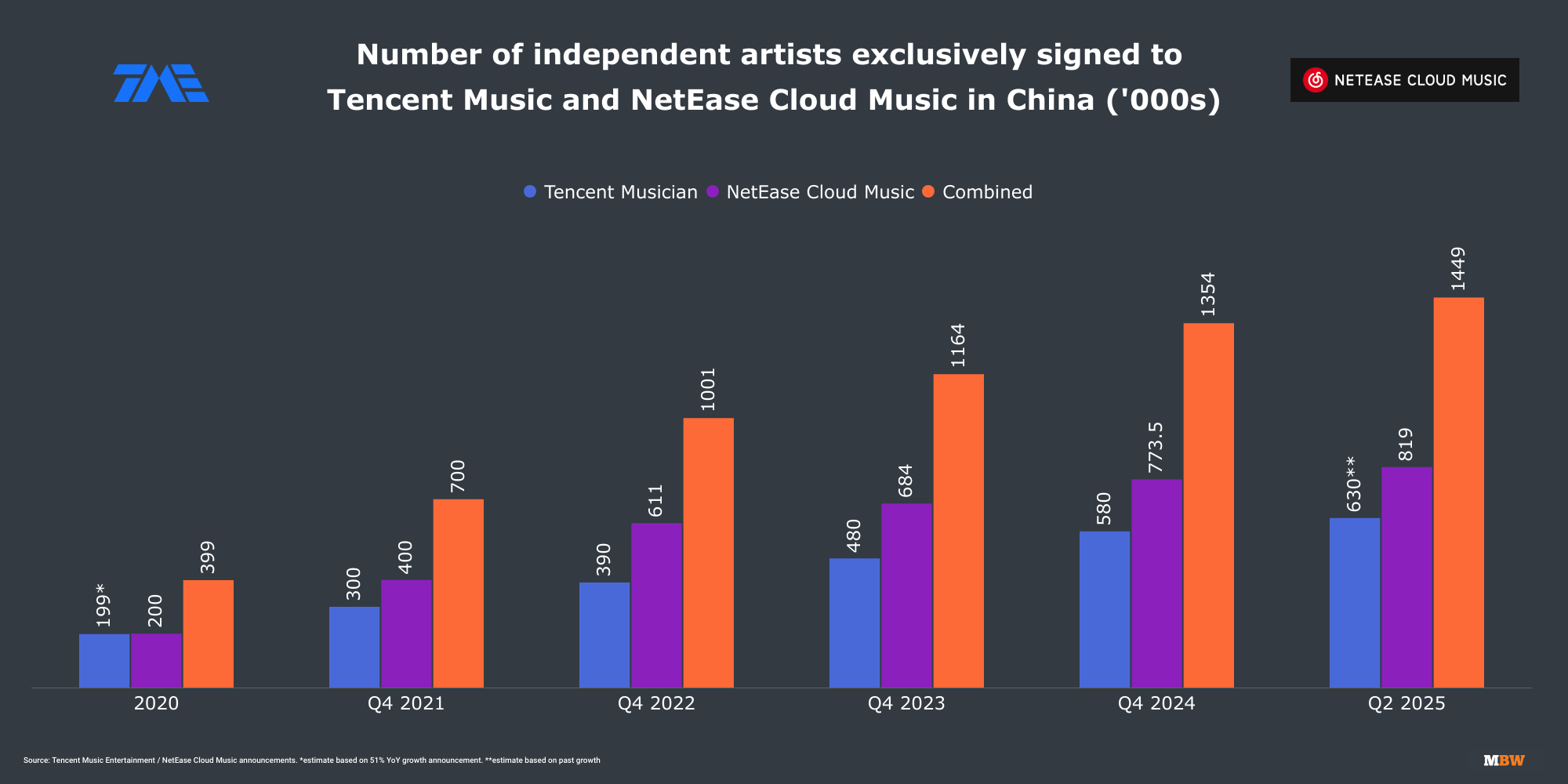

According to financial filings reviewed by MBW, some 1.4 million artists are now signed directly to the ‘independent’ distribution/label services arm of either Tencent Music or NetEase Cloud Music.

These indie artists don’t just release music via TME/NetEase.

The hottest acts also receive a host of career-accelerating benefits – including music-making assistance and serious marketing support.

{kind=link}

In Tencent Music’s latest quarterly filing (Q2 2025), the platform highlights its “cross-platform promotions” for several key tracks signed to DIY artist services arm, Tencent Musician.

One of these tracks – Xiang Sisi’s Why Not Wait for the Wind – amassed over 20 million streams and “topped multiple music charts” in Q2.

In addition, TME facilitated over 300 live performance opportunities in the quarter for nearly 100 of its directly-signed artists.

Meanwhile, NetEase Cloud Music has signed a whopping 819,000 indie artists to date, who’ve released 4.8 million tracks between them.

A number of these NetEase-signed acts have received label-like services including financing (via ‘Cloud Ladder’), plus invitations to sync music in ad campaigns for major brands.

NetEase-signed artists also receive A&R resources, whether digitally (‘AI Musician’ and ‘Trainee Musician’) or via offline songwriting camps.

Since 2021 says NetEase, its nine songwriting camps have produced 120 tracks that have “collectively garnered more than 6 billion plays”.

Concurrently, NetEase is making its own music via “in-house studios”. These studios have apparently “produced and popularized multiple hit songs across our community and external platforms”.

NetEase doesn’t make clear in earnings reports whether these “hit songs” are performed by human artists (or not). However, it recently confirmed its biggest “in-house” hit of calendar Q2: Liang Nan (两难).

Through the wonder of Google Translate, I’ve tracked it down… and it’s Bieber-esque:

The growing scale of Tencent and NetEase’s self-signed hits is obviously not ideal for ‘western’ companies looking to secure global market share. Especially as China continues its ascent towards becoming the world’s second-biggest subscription music market.

In calendar Q1, Warner Music Group announced underwhelming growth in global streaming revenues (+3.2% YoY).

Oddly, this happened despite major US-driven frontline successes at Atlantic Music Group and Warner Records. WMG CEO Robert Kyncl even confirmed the quarter was defined by “our strongest [US] chart presence in two years”.

What dragged down Warner’s global numbers? The China Paradox was an important factor.

As WMG told investors: “Streaming revenue was [affected] by a lighter release slate and market share loss in China.”

Sources suggest this market share loss was partly due to WMG’s general underperformance in China – significantly exacerbated by the popularity of TME and NetEase’s own artists.

Warner is now banking on an executive with strong local knowledge and connections to remedy its decline in China.

The appointment of WMG’s new Hong Kong-based APAC chief, Lo Ting-Fai, was confirmed alongside the firm’s much-stronger calendar Q2 results in August.

Robert Kyncl said that Ting-Fai will be “committed to finding and developing artists with massive creative and commercial impact” while “growing our market share across the [APAC] region”.

Warner’s wobble in the face of ‘The China Paradox’ is not unique.

Higher-ups at other significant music firms have quietly noted similar concerns in private conversations – while also voicing worries over AI-assisted music being encouraged by TME and NetEase on their platforms.

It hasn’t gone unnoticed, for example, that Tencent Music –partly via an integration with copyright-ignoring AI platform DeepSeek – now enables its users to make AI tracks and upload them directly to flagship music service, QQ Music.

The strategic response

So how do large music rightsholders navigate this new reality in China?

One response, as seen by WMG’s Lo Ting-Fai appointment, is to recognize that success in China requires local expertise, relationships, and cultural understanding – not just catalog licensing.

I suspect, at some stage, deeper partnerships with Tencent and NetEase may also have to be struck.

Rather than treating Chinese platforms as simple licensees, Western labels may increasingly explore joint ventures and co-production deals.

The torchbearer for this model is Universal Music Group and Tencent, who have been tied together since a Tencent-led consortium finalized the acquisition of a 20% stake in UMG four years ago.

Even before that deal was signed, UMG and Tencent Music established JV label operations in China, with the intention of “cultivating, developing, producing, and showcasing highly talented domestic artists”.

Boosted by the market expertise that evolved from this setup, UMG has seen positive commercial results in China of late – even against the backdrop of TME/NetEase’s growing in-house music roster.

In April, UMG confirmed “double-digit growth” in China, while praising the conversion of free users into paid users by the likes of Tencent.

Back in 2021, as UMG was welcoming Tencent to its cap table, we saw a run of other music companies inking more straightforward licensing deals with Chinese platforms.

They included indie rights rep Merlin, announcing a fresh multi-year agreement with NetEase.

Merlin’s then-CEO, Jeremy Sirota, commented that the deal showed “independent music is a real focus across the world, including in China”.

He couldn’t have been more right.

Today, NetEase and Tencent seem extremely focused on independent music – so long as it’s signed directly to them.Music Business Worldwide